Market Design

Signals v1 is built for continuous outcomes. Instead of forcing a question into binary choices, the protocol represents the outcome as a grid of discrete ticks and lets traders buy ranges on that grid. This keeps continuous questions tradable while preserving a clean settlement surface.

The grid is not a UI trick. It is the contract between the real world and the on-chain mechanism. Without it, settlement would be ambiguous, payouts would be disputable, and the market would collapse into interpretation. With it, every outcome has a single on-chain meaning.

The grid also guards against measurement ambiguity. Real-world feeds are noisy and timestamps are discrete. A deterministic mapping from values to ticks means that two independent observers can arrive at the same settlement tick without negotiation. That is the prerequisite for an on-chain market that does not depend on interpretation.

Because ranges are standardized claims on intervals, the grid makes continuous beliefs composable. Traders can express a wide range of views by combining ranges, and the pricing curve can evaluate all of those views on the same shared state. That is the foundation for a market that is both expressive and coherent.

The grid is a settlement contract

On-chain settlement needs a finite set of states. The outcome grid is that finite set: every real-world value maps to exactly one tick, and every tick corresponds to a single payout rule. This mapping is what makes settlement objective rather than negotiable.

Put differently, the grid answers the hardest question before trading starts: “If the world ends up at value X, what happens on-chain?” Once that question has an unambiguous answer, trading can be fair because everyone is trading over the same payout map.

The grid also fixes boundary behavior. The protocol uses half-open intervals so that adjacent ranges do not overlap at their boundaries. That small convention removes an entire class of double-counting disputes at settlement.

In practice, the grid turns a messy real-world measurement into a single settlement index. The market does not need to argue about the exact value, only which tick it falls into. A continuous market still needs discrete structure at the final step.

Resolution is a tradeoff, not a magic dial

Tick spacing is the market's resolution. A tighter grid means more precision, but it also means more ticks, which changes how price impact and liquidity are felt across the curve. A coarser grid is cheaper to move but less precise. Resolution is the first and most concrete tradeoff in a continuous market.

Think of it like a camera sensor. Higher resolution captures finer detail, but it also increases the number of pixels the system must process. In a market, more ticks mean more states to price and a different shape to price impact. That Resolution is not just a UX choice; it is a structural choice.

Concrete consequence: resolution determines how “thin” or “thick” a range is in tick terms. A narrow range in a fine grid can behave very differently from a narrow range in a coarse grid, even if the real-world width is the same.

Resolution also sets the size of the minimum settlement error. If the real world measurement is noisy at, say, ±s, then a grid much finer than s adds precision that the data cannot support. Conversely, a coarse grid can introduce discretization error that traders will price into ranges. The grid makes that error explicit rather than implicit.

Finally, resolution interacts with depth. For a fixed depth, spreading probability mass across more ticks means each tick is thinner, so moving price mass over a narrow range can feel more sensitive. That coupling between tick spacing and price impact is a core design lever.

How the mapping works

The outcome domain is an interval divided into evenly spaced ticks of size . Each tick represents a bucket of outcomes. An observed value maps to a single tick by clamping and flooring:

This is the mechanism's promise: any real-world value lands on one and only one settlement tick. The rule is deterministic and testable. Given an outcome value, the settlement tick is computable from the rule, and the on-chain result must match that mapping.

That determinism is what makes settlement objective. If the data feed and the mapping rule are known, the settlement tick is not subjective.

The clamp step defines out-of-range behavior. Values below L map to the first

tick; values above U map to the last. That behavior makes the market's domain explicit and

removes ambiguity about out-of-range values. When the bounds are clear, the

rules for extreme outcomes are clear too.

The inverse mapping is also simple. A tick index corresponds to a value interval:

This is the content of "tick meaning." It turns settlement into membership in a finite set of half-open buckets. When a market settles, it is not settling to a real number. It is selecting one of these buckets and committing to it on-chain.

Spacing alignment is part of the behavioral surface. Tick boundaries are defined in units of . A range boundary that is not aligned to spacing is not a valid boundary in the mechanism model, because it does not correspond to a clean set of tick buckets.

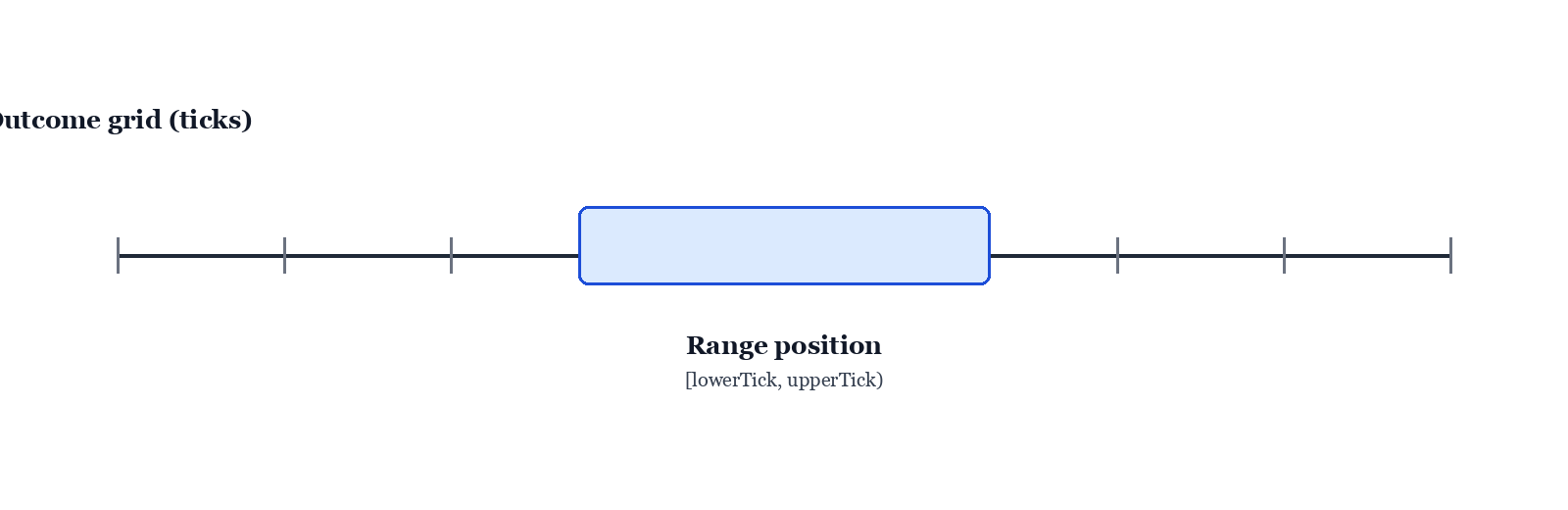

Range positions are the primitive

A position is a contiguous interval on the grid. If the final settlement tick falls inside that interval, the position pays a fixed quantity. If it falls outside, the payout is zero. This makes a range position behave like a binary event over “in the range” vs “out of the range,” while still capturing continuous outcomes.

Figure: A range position highlights a contiguous interval on the outcome grid.

That binary-like payout is not a limitation. It is the reason the market is analyzable. Continuous beliefs can be expressed without inventing a new instrument each time. The range itself is the instrument.

Another way to see it: a range position is a standardized claim on an interval. Standardization is what allows a single curve to price all ranges consistently. Without that standard form, every interval would behave like a bespoke contract.

Because ranges are standard, they can be composed. A trader who wants a triangular or bell-shaped belief can approximate it by combining adjacent ranges with different sizes. This is how a continuous belief becomes a bundle of standardized positions, each priced by the same curve.

Range positions also have a natural complement. Holding the full domain range behaves like a constant payout position. Combining a specific range with its complement in the domain yields a constant payoff across the full domain. This is another way to see why half-open semantics matter: the complement is well defined only when boundaries do not overlap.

A concrete example

Suppose the outcome domain is with tick spacing . The range spans 20 ticks. A settlement price of maps inside the range and pays out the position's quantity. A price of maps outside and pays out zero. The rule is simple; the complexity is in pricing the range fairly, which is handled by the shared CLMSR curve.

This example reveals the market’s geometry: the same position is a bundle of 20 adjacent ticks, and its payout depends only on the final tick. That geometry is what makes the market analyzable rather than ad hoc.

It also highlights the boundary rule. A settlement price exactly at maps to the first tick above the range, not the last tick inside it. That is the half-open interval convention in action.

Out-of-range behavior is equally explicit. If the market domain is and a settlement value lands below , it clamps into the first tick. If it lands at or above , it clamps into the last tick. These are not special cases in the implementation. They are the direct result of the clamp in the tick mapping rule.

In practice, a single narrow range behaves like a "resolution-limited point bet." As the range shrinks in tick terms, the cost rises because the trade is concentrating probability mass into fewer ticks. The curve prices that precision and makes the cost measurable.

Tick spacing sets a tradeoff. Coarser grids reduce the number of ticks, which often lowers price impact for a given notional size but also reduces settlement precision. Finer grids increase precision but make narrow ranges more expensive to move. The mapping rule is deterministic, so settlement disputes are about data, not interpretation.

Related sections: